Contingent Property:

A Contingent Asset is an financial acquire which will come into existence in close to future on account of some previous motion. The existence of such belongings is totally unsure and past the management of the entity.

Instance: Any property of a agency underneath some authorized swimsuit, and guarantee acquired by a agency.

Contingent Liabilities:

A Contingent Legal responsibility is a legal responsibility, the existence of which relies upon upon the occurring of some future occasions. Like Contingent Property, Contingent Liabilities are unsure and past the management of the entity.

Instance: Any compensation prone to be paid in close to future on account of some lawsuit, guarantee given by the agency, discounting, or endorsement of payments.

Accounting Remedy of Contingent Property:

(i) Contingent Property realised for Money:

A Contingent Asset, if any, like every other asset is transferred to the credit score facet of a Realisation Account on being realised for money.

Journal Entry:

(ii) If any of the companions take over Contingent Property and agrees to pay for a similar:

A Contingent Asset when taken over by a associate, is transferred to the credit score facet of a Realisation Account and debited to Involved Companion’s Capital Account.

Journal Entry:

Accounting Remedy of Contingent Liabilities:

(i) Contingent Liabilities paid off:

Like every other legal responsibility, the Contingent Legal responsibility can also be paid off and is transferred to the debit facet of a Realisation Account.

Journal Entry:

(ii) If any of the companions agrees to settle a Contingent Legal responsibility:

A Contingent Legal responsibility when taken over by a associate, is transferred to the debit facet of a Realisation Account and credited to Involved Companion’s Capital Account.

Journal Entry:

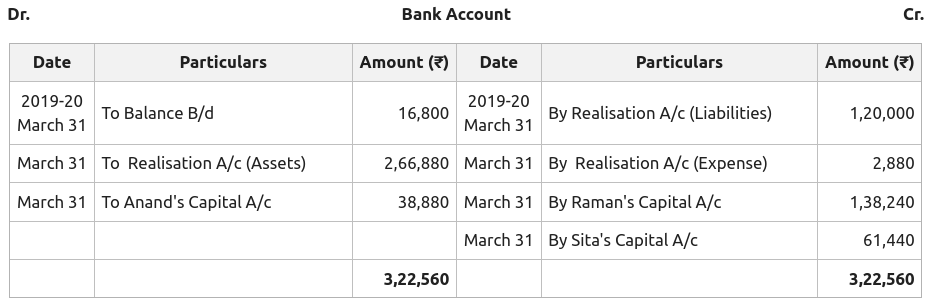

Illustration:

Raman, Sita and Anand have been companions sharing Revenue within the ratio of two : 2 : 1. Their Steadiness Sheet on thirty first March 2020 stood as:

Further Info:

1. Property realised as:

Inventory – ₹ 67,200

Debtors – 90% of worth

Equipment – ₹ 1,32,000

2. Sita took over the Funding at ₹ 28,800 and likewise agrees to pay the excellent wage.

3. Patents have been worthless.

4. A Invoice Receivable of ₹ 7,200 was discounted from a financial institution, however on the due date, the Buyer grow to be bancrupt and paid solely 70 paise in a rupee.

5. Collectors realised for ₹ 64,800.

6. Realisation bills amounted to ₹ 2,880.

Put together Realisation Account, Companion’s Mortgage Account, Companion’s Capital Account and Money Account and move obligatory Journal Entries.

Resolution:

Working Notes:

1. Complete Realised Worth of Property:

Inventory = 67,200

Debtors = 62,640

Equipment = 1,32,000

Invoice Receivable (Contingent Asset) = 5,040

Complete = 2,66,880

2. Complete Laibilities Realised:

Collectors = 64,800

Invoice Receivable

(Contingent Legal responsibility) = 7,200

Quick-term Mortgage = 48,000

Complete = 1,20,000

Notice: Full worth of the Invoice Receivable is taken into account as Contingent Legal responsibility as a result of the complete quantity is to be returned to the Financial institution. Nevertheless, 70% of it’s acquired therefore that half is taken into account as Contingent Asset.