What’s Joint Life Coverage?

Joint Life Coverage is a life coverage that offers protection in opposition to the loss of life of the policyholder, underneath which the protection is of a minimal of two individuals and the pay-out is on a first-death foundation. Because the Partnership agency is a enterprise run by at the least two individuals, the companions could maintain the Joint Life Coverage in an effort to cut back the burden of paying a significantly great amount within the occasion of retirement or loss of life of the associate or Dissolution of the partnership. If any associate dies earlier than the maturity date of the coverage, the opposite companions are eligible to obtain the coverage quantity (Full Declare).

Accounting Therapy:

Case 1: If Joint Life Coverage seems within the Steadiness Sheet:

When a Joint Life Coverage seems within the Steadiness Sheet, it’s transferred to the Realisation Account’s debit aspect, like another asset at its guide worth.

Illustration:

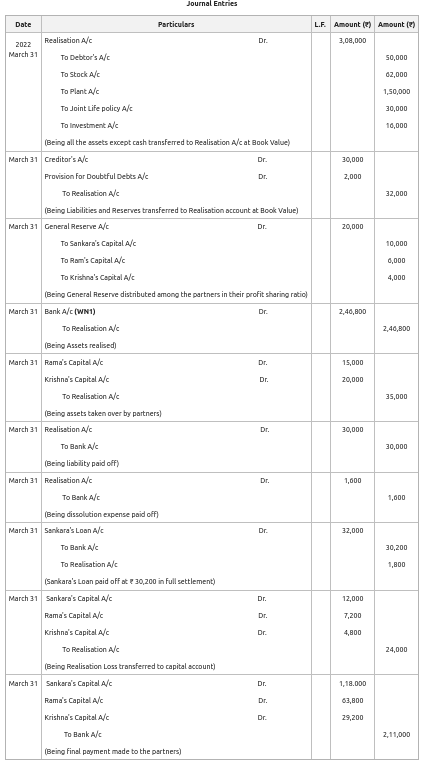

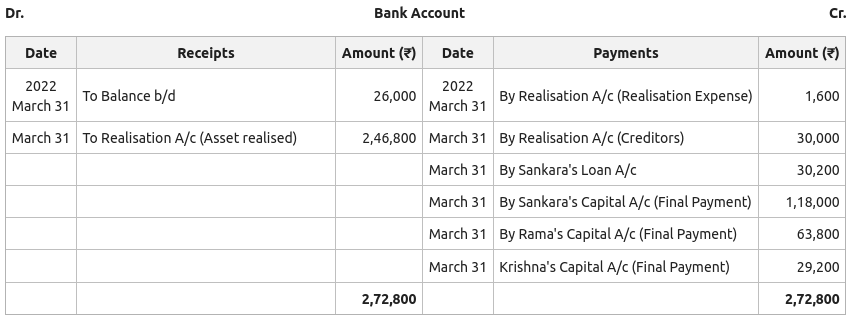

Sankara, Rama, and Krishna had been companions for five:3:2 in a agency. Their Steadiness Sheet on thirty first March 2022 stood as:

The companions resolve to dissolve the agency on the identical date underneath the followings circumstances:

- The Investments are taken over by Rama at ₹ 15,000.

- Joint Life Coverage was surrendered for ₹ 20,000.

- The plant was offered for ₹ 1,27,200.

- The inventory was offered for ₹ 84,000.

- Krishna took over debtors price ₹ 24,000 for 20,000. The remaining debtors had been realised at 60% of the guide worth.

- Sankara’s Mortgage was cleared by paying ₹ 30,200 in full settlement.

- Dissolution bills price ₹ 1,600.

Move vital Journal Entries and put together vital accounts to shut the books of the agency.

Resolution:

Working Observe:

1. Worth of Asset Realised:

Joint Life Coverage – 20,000

Inventory – 84,000

Plant – 1,27,200

Debtors –

Complete – 2,46,800

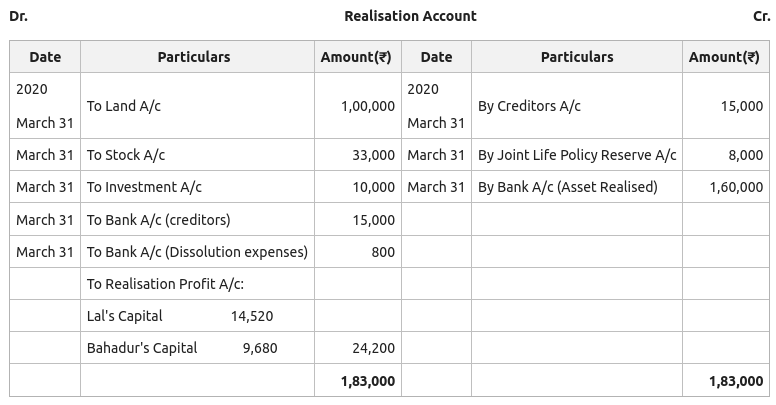

Case 2: If Joint Life Coverage reserves additionally seem within the Steadiness Sheet:

Below this case, the Joint Life Coverage reserves are transferred to the credit score aspect of the Realisation Account.

Illustration:

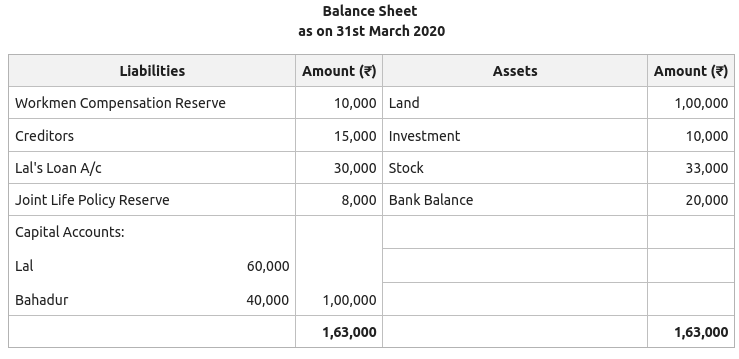

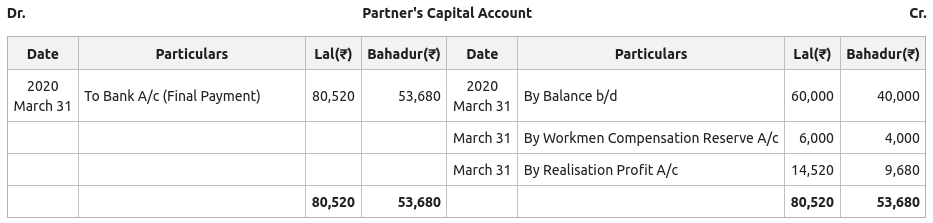

Lal and Bahadur had been companions sharing revenue within the ratio of three:2. On thirty first March 2020, they determined to finish the partnership and proceed in the direction of dissolution. On the identical date, their Steadiness Sheet stood as:

Further Data:

- The land is offered at 20% revenue.

- Funding is realised at guide worth.

- Inventory is realised at ₹ 30,000.

- All of the liabilities together with the associate mortgage are paid off.

- Dissolution Bills amounted to ₹ 800.

Move vital Journal Entries and put together vital accounts to shut the books of the agency.

Resolution:

Case 3: Quantity acquired from the Insurance coverage Firm on give up of the coverage:

Below this case, no matter quantity is acquired from the Insurance coverage Firm on the give up of the coverage, is credited to the Realisation Account.

Illustration:

The Steadiness Sheet of Rahul, Ravi and Raman on thirty first March, 2018 stood as:

Further Data:

- Debtors realised at ₹ 16,800 and Collectors and Invoice Payable was paid at a reduction of 10%. Brief-term Mortgage paid.

- Inventory was taken over by Raman for ₹ 9,000 and furnishings was offered for ₹ 7,200.

- Land and Constructing had been offered for ₹ 1,68,000.

- Unrecorded asset price ₹ 12,000 was realised at ₹ 8,400.

- The agency had a Joint Life Coverage of ₹ 3,00,000 with a give up worth of ₹ 51,600. The coverage was surrendered on the identical worth.

Move vital Journal Entries and put together vital accounts to shut the books of the agency.

Resolution:

Working Observe:

1. Worth of Asset Realised:

Joint Life Coverage – 51,600

Land and Constructing – 1,68,000

Debtors – 16,800

Furnishings – 7,200

Unrecorded Asset – 8,400

Complete – 2,52,200

2. Worth of Liablities Paid off:

Collectors –

Payments payable –

Brief-term Mortgage – 7,200

Complete – 39,600